Introduction to Business Valuation (CFI)

https://corporatefinanceinstitute.com/course/intro-business-valuation/

https://www.credential.net/6424b711-a689-4088-b6f7-4e389cedff20

The examples and spreadsheets included in the course are super useful! All also available here: https://learn.corporatefinanceinstitute.com/resources/templates/

General Corporate Finance

Asset valuation technique (based on replacement cost, liquidation value) isn’t used much so not in this course

Enterprise value (assets) = equity value (market cap = shares * price) + net debt (debt - cash)

Capital structure = debt to equity ratio

Payment order: vendors/employees (COGS) → debt holders (interest) → government (tax) → shareholders (net earnings)

Enterprise value and equity value both have pros and cons for valuation

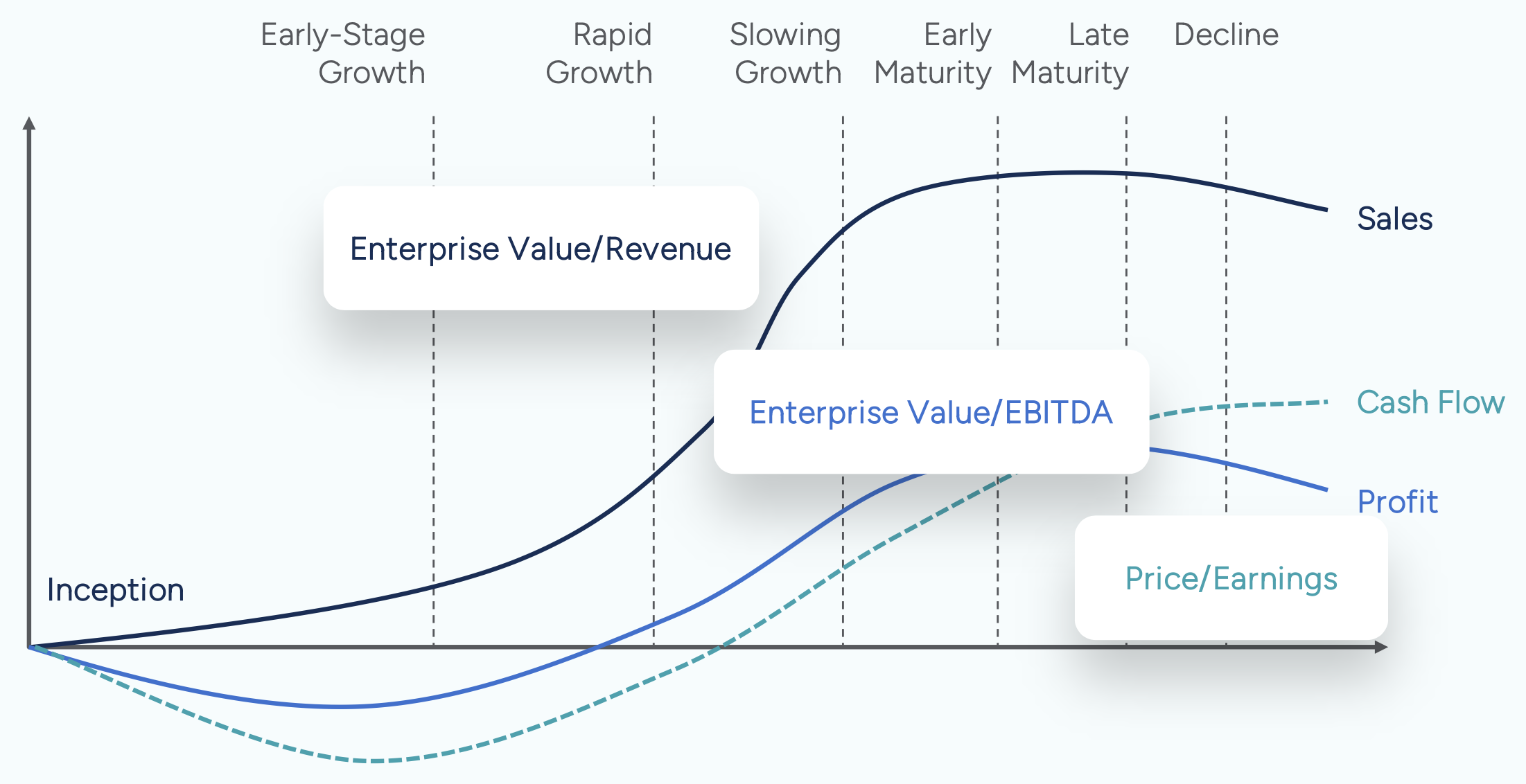

If metric is pre-interest, use enterprise value multiple (as unaffected by capital structure): EV/sales, EV/EBIDTA, EV/EBIT

If metric is post-interest, use equity value multiple (affected by capital structure due to interest payments): P/E, P/B

DCF Valuation

Pros and Cons

| Pros | Cons |

|---|---|

| Theoretically most correct | Only as good as the inputs (of which there are many) |

| Opportunity to learn about the company/industry | Easier to manipulate (by adjusting inputs) |

| Less prone to market conditions | Complex doesn’t necessarily mean precise |

Free Cash Flow

Unlevered free cash flow (UFCF)

- A.k.a. free cash flow to the firm

- Before paying debt

- More common

- DCF derives EV

- Use WACC

Levered free cash flow (LFCF)

- After met debt obligations

Difficulties

- Hard to estimate discount rate for private company

- Hard for young or financially distressed companies

Stage 1: forecast; stage 2: terminal value

UFCF =

- EBIT * (1 - tax rate) + depreciation and amortisation - capital expenditures - net increase in working capital

- Note: EBIT (aka operating income) * (1-tax rate) = net operating profit after tax (NOPAT)

- Net income + after-tax interest expense (interest expense * (1 - tax)) + depreciation and amortisation - capital expenditures - net increase in working capital

- EBITDA - unlevered cash tax (note: harder to get) - capital expenditures - net increase in working capital

WACC

- Yield not coupon

- Yield * (1 - tax rate)

Capital Asset Pricing Model (CAPM)

- Risk-free rate (e.g. yield of long-term govt bond) + premium (beta [change in stock return vs overall market] * equity risk premium)

- Alpha = firm-specific risk

- Diversification of stocks removes alpha within a portfolio

- Beta = market risk (beta of market = 1)

- If company has beta of 1.25 then it is riskier than the market → market +/- 1%, stock +/- 1.25%

- Return vs risk graph shows risk premium

- R-squared correlates stock and market → if too low, better to use industry beta

- Industry beta → unlever beta (levered beta / (1+(1-tax rate) * (debt/equity)) → average → relever beta (unlevered beta * (1+(1-tax rate)*(debt/equity))

Terminal Value

Note: Both must discounted back to present value

Note: Assume last day of fiscal year

Perpetuity Growth Method

TV = Last forecast UFCF * (1 + g) / (WACC - g)

Note: g is often market growth rate

Terminal Multiple Method

TV = Last forecast EBITDA * EV/EBIDTA

Note: Not always EBITDA, but commonly

NPV

=NPV(rate,values_1,value_n)

Assumptions

- Discounts all cash flows

- Occur at regular intervals

- Occur at end of the period/year

For cash flow occurring in middle of period/year: =NPV(rate,values_1,value_n)*(1+rate)^0.5

XNPV

=XNPV(rate,value,dates)

Assumptions

- Initial cash flow is not discounted

- Occur at regular intervals

- On a daily basis

Slightly more accurate because of leap years

IRR

Discount rate when NPV = 0 (hurdle rate)

IRR > CoC, profitable → invest!

=IRR(values,[guess])

Assumptions

- At least one positive and one negative value

XIRR

=XIRR(values,dates,[guess])

Assumptions

- First value is usually negative

- Values in chronological order

- Dates correspond to the periodic cash flows

Slightly more accurate because of leap years

Relative Valuation

Comparable Companies or Precedent Deals

Pros and Cons

| Pros | Cons |

|---|---|

| Simple | Can be too simplistic |

| Observable data | All companies are different |

| Reflects current market conditions | |

| For M&A, can show premium |

Multiples

Multiples affected by

- Growth rates

- Management team

- Mispricing

- Accounting policies

- For precendents:

- Age of deal

- Lack of deals

| Multiple | Pros | Cons |

|---|---|---|

| EV/Revenue | Younger companies haven’t reached profitability | Doesn’t account for costs Revenue is an incomplete measure of performance |

| EV/EBITDA | Commonly used Used for industries with large amounts of long-term assets |

Net income is the bottom line EBITDA doesn’t include reinvestment |

| P/E | Used for mature, publicly traded companies | Demoniator based on accrual accounting which can be manipulated |

| P/B | Used for banks | Limited usefulness for non-banks |

Process

-

Select companies for similar:

- Industry

- Geographical location

- Size and growth profiles

- Profitability

- Accounting policies

- Capital structure

- Extra for precendents

- Recent deals

- Buyer

- Strategic buyer will pay more to benefit from synergies

- PE buyer will pay less as no synergies to be gained

Capital IQ can provide this data

-

Enter data

- Note: Purchase price is effectively EV for precedent valuation

-

Value using multiples

Football Field Chart

x = valuation techniques, y = value

- Create table: min, midpoint, max for each valuation method

- Create stacked column

- No fill for max and min

- Data labels for max and min

- Average valuation = manually drawn line

- Textbox with formula (TEXT function for formatting)